Before you set your advocacy objectives, you will need to analyse the external context. Which are the institutions, organisations and individuals that you need to influence to bring about the change you are seeking? What is the political context that you are operating in and how will this influence the approach you take to your advocacy? What are the upcoming opportunities that you should take into account? This section provides some tips.

Do your power analysis

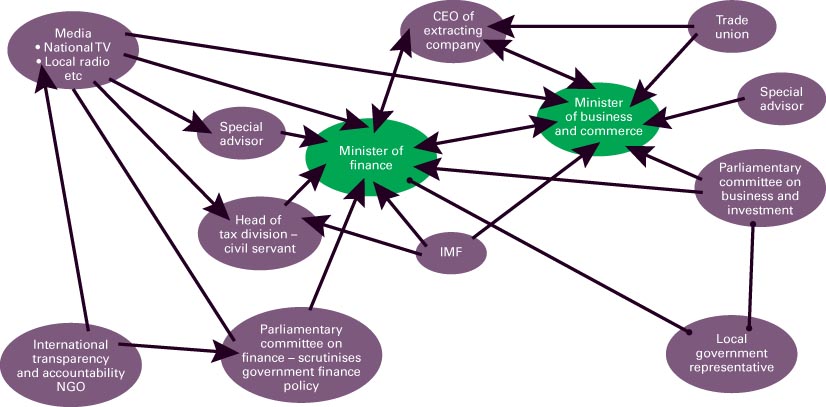

In essence, a power analysis is about capturing who has the most power to bring about the change you want to see and who in turn has influence over them. This will help you identify where and at which institutions or individuals you should target your advocacy.

TOOLPower map/analysis

For example, if one of your concerns is to ensure that civil society in your country has access to information

The power map will help you identify the targets for your advocacy. Targets can then be broken down into:

- primary targets (those with the most direct influence)

- secondary targets (those with influence over the primary targets, or those with some influence on the issue but not as much as the primary targets). These secondary targets are sometimes referred to as ‘influentials’. Influentials can be found in a variety of places, and not just among those officially part of a decision-maker’s immediate circle. They include the media, members of parliament, donors, faith leaders, other government departments and trade unions.5

Identify your tax stakeholders

As with most things in life there’s more than one way to do it! For example, eating an apple – you can slice it, dice it, discard the peel; or munch it whole, seeds, peel and all. The same applies to advocacy planning tools. The power map will help you identify primary and secondary targets for your advocacy. Meanwhile a stakeholder analysis will help you identify a broader set of stakeholders – not just the targets but also potential allies and opponents.

A stakeholder analysis will help you identify ‘who’ you should be speaking to and who you need to work with in order to achieve the change you’ve identified. These people are usually referred to as stakeholders because they have an interest or ‘stake’ in the issue.

This section provides tools to help you do a stakeholder analysis.

Types of stakeholders usually break down into the following categories:

- Targets: they are decision-makers, people who have the power to make the desired changes, or people with influence over decision-makers. Some decision-makers can turn out to be allies, so don’t automatically think of them as opponents.

- Constituents: the people you work with and for, who are directly affected by the situation and can be expected to benefit from your advocacy.

- Allies: those who share your aims and can help to influence or put pressure on the decision-makers. Allies could be CSOs, churches, media, non-governmental organisations (NGOs), businesses, etc. They may even turn out to be decision-makers if you’re lucky!

- Opponents: those who are opposed to what you want to achieve and will try to block the changes you want to see.

NB: Remember that your analysis of an institution needs to be subdivided as there may be allies, opponents or targets within one institution.

Before we outline the different tools for mapping stakeholders and analysing their power and influence over the decision-making process, let’s take a look at some stakeholders that are particularly relevant to tax work.

The ‘Who’s Who’ of tax stakeholders

Communities and citizens

Because tax justice helps enable the provision of basic services and the achievement of greater equity, everyone is a stakeholder in tax justice campaigning. Because everyone is affected by low revenue or unfair distribution, you can address everyone in your community through your tax campaign.

Taxpayers

Taxpayers are not all the same, and thus they should be treated according to their capacity, and their type of activity. Taxpayers include both companies and individuals and they pay taxes directly on their income and/or indirectly, for example on goods and services. Even the poorest people in society are taxpayers through their consumption.

States offer different tax treatment to taxpayers based on their income or capacity to pay, some systems being more progressive and others highly regressive.

Taxpayers themselves are possibly the most important stakeholders, as citizens who are aware of their role as taxpayers can form interest groups and demand transparency in using their tax money.

Governments

Governments, local and national, are responsible for developing and implementing domestic tax policy. Tax is a vital source of revenue for most governments so, like tax justice advocates, they do have an interest in ensuring that tax is collected. However, their approaches to how taxes should be raised often differ from those of tax justice campaigners, as many governments have tended to support tax formulas that are not progressive. This is why tax justice advocates the world over are trying to influence their governments to introduce more equitable national tax policies.

Many governments also have a role in negotiating international dimensions of tax policy. In some countries, tax justice campaigners are urging their governments to take a stronger stance in the G20, or as part of the G77, to push for more transparent accountancy rules for multinational companies (MNCs) internationally.

With regard to MNC taxation, different parts of governments may have different approaches. The parts dealing with investment promotion will favour a low-tax environment to reduce MNCs’ tax liability. Those dealing with tax revenue generation may oppose this. Understanding the positions of different political figures and their departments is therefore important for tax justice advocates.

Revenue authorities and tax administrators

In some countries, tax authorities are independent of government, with their own budgets and salary scales. (In others, they are typically a part of the ministry of finance.) Independent tax authorities are usually better resourced, and their staff better paid, than other government departments, because they compete with the private sector for their staff. But tax authorities in southern countries are still severely underfunded in comparison to their northern equivalents, facing real capacity constraints, often leading to low morale among staff and sometimes corruption. It is hard enough for these authorities to audit the accounts of domestic companies that may be trying to evade tax, let alone to penetrate the complex accounts of MNCs and spot if they are reallocating profit and loss among subsidiaries in order to evade tax.

- African Tax Administration Forum (ATAF): this new

body, launched in 2009, brings together 25 African tax administration bodies. ATAF’s mission is to mobilise domestic resources more effectively and increase the accountability of African states to African citizens while actively promoting an improvement in tax administration through sharing experiences, benchmarking and peer reviewing best practices. ATAF’s communiqué can be found at www.oecd.org/dataoecd/31/48/44109654.pdf - Asia Tax Forum: according to its website, ‘The Asia Tax Forum regularly brings together senior government officials with leading fiscal experts and industry representatives. Its goal is to create a sustainable and continuing dialogue among all interested sectors on latest developments, studies, issues and challenges on indirect taxation. The forum focuses on the VAT and excise taxation.’ See www.asiataxforum.org

The real frustrations that they face mean that tax administrators are often more supportive of tax justice advocates than the average civil servant, and willing to build relationships with tax justice advocates. By sharing tax research and proposals for more transparent and equitable tax systems, this could indirectly influence the governments of the tax administrators you are targeting – depending on the relationship between the administrators and the politicians in your country.

Multinational companies

MNCs are major economic players and providers of employment and income in most southern countries. In addition, taxes from MNCs are a vital source of revenue, enabling governments to provide the services to which their citizens are entitled. However, MNCs have tended to demand, and have received, major tax concessions from governments as the price for setting up operations – and governments worry that investment will go elsewhere if such concessions are not offered. Such tax breaks represent a huge cost to southern governments’ coffers. Certain unscrupulous MNCs also engage in tax avoidance and evasion of the kind described in Chapter 1, which further drastically reduces the potential tax revenue for southern governments. Christian Aid estimates that such trade mispricing alone costs the developing world US$160 billion in lost tax revenues every year.6

MNCs are made up of subsidiary companies. Corporate structures differ, so while the subsidiary in your country may be under close control from the MNC’s head office, in other cases it could have considerable autonomy and a local staff team. In many cases, subsidiaries are listed on the stock exchange, and there are significant local shareholders who lose out from profit shifting that reduces their dividends – and who may therefore be allies of tax justice advocates.

Accountants and accountancy bodies

Accounting companies can be anything from offices with one single accountant that provide vital services to small and medium sized enterprises (SMEs), to large national providers of accounting and payroll services. Every registered company over a certain minimum threshold needs to prepare accounts; over a certain threshold they also need to be audited. Accountants provide both services.

Some accounting companies also offer services that allow their clients to avoid or evade taxes.

- The Big Four: the most influential among these are the so-called ‘Big Four’ accountancy firms: Deloitte, KPMG, Ernst & Young and PricewaterhouseCoopers. They all operate in almost all countries, and in most tax havens. Multinationals prepare their accounts with them, as do many national companies who are active in foreign trade. Tax justice advocates can target the Big Four directly, or urge their client companies to exert influence.

Most if not all accountants are members of professional associations such as Institutes of Chartered Accountants; and national branches of global accountancy bodies such as the Association of Chartered Certified Accountants (ACCA) and the Federation of Francophone Certified Accountants (FIDEF). Some of these associations provide capacity-building programmes for accountants and government auditors in southern countries. These associations are represented in the International Accounting Standards Board (IASB) and

its associated bodies (see below). Being membership associations they can adopt motions put forward by their members – so tax justice advocates could build alliances with these national bodies.

The International Accounting Standards Board

The IASB is the body of accountants that devises the rules covering how companies should produce their annual accounts. More than 100 governments worldwide tend to rubber-stamp their findings into law. Currently, MNCs only publish global accounts, which makes it incredibly difficult for tax authorities in developing countries to identify where MNCs are making their profits and therefore how much tax these companies should pay in their country. This lack of transparency enables MNCs to minimise their tax payments through a variety of creative accounting mechanisms. Organisations campaigning for tax justice have been targeting the IASB to call for a country-by-country reporting standard.

At the time of producing this toolkit, the IASB was conducting a consultation on proposals for a country-by-country reporting standard in the extractives sector.

Secrecy jurisdiction governments

As a key component of sovereignty is the ability to raise revenue, states that provide financial secrecy undermine the ability of other states to do this. Also known as tax havens, these states or autonomous territories provide secretive financial services for non-resident companies, causing vast tax losses for developing and developed countries alike on wealth hidden away from tax authorities. Secrecy jurisdictions raise significant revenue from annual registration fees on secret companies, while local residents often pay high indirect taxes, and some direct tax. Not all secrecy jurisdictions provide the same levels of secrecy and some are worse than others. Meanwhile, residents of many secrecy jurisdictions would like to find an exit strategy from the secrecy trade.

International Monetary Fund

The IMF exerts a powerful influence on developing country economic policy formulation, including on approaches to taxation. In the past, through conditions attached to its loans and the influence of its reports on investor confidence, the IMF has been able to effectively promote the ‘tax consensus’ that was discussed in Chapter 1. This has involved reductions in the rates of corporate taxation, including far-reaching tax breaks for foreign investors, reductions in export and import taxation through trade liberalisation, and the introduction or expansion of (often regressive) sales taxes such as VAT.7

Recent evidence suggests that the IMF now takes a more nuanced position on these issues.

World Bank

The World Bank pursues a similar agenda to the IMF through its influence on developing country economic policy. Particularly influential is its Doing Business rankings

(www.doingbusiness.org) which governments the world over use as a yardstick for measuring their business and economic policy. The rankings take into account the time and effort needed to form and maintain a company, encouraging governments to eliminate ‘red tape’; but they also include indicators on tax policy.

Organisation for Economic Co-operation and Development (OECD)

The OECD is a group of around 30 of the world’s richest, most powerful democracies. Based in Paris, the secretariat has adopted tax policy and administration as a core function. This includes organising advice and technical assistance for developing countries.

The OECD is also an international standard-setter on tax policy: its transfer-pricing guidelines are used by tax authorities to assess companies’ profit-shifting activities, and its model tax treaties form the basis of bilateral agreements on tax cooperation and information exchange. Global standards used to assess tax havens are set, and assessments made, by the OECD’s Global Forum on Transparency and Exchange of Information for Tax Purposes. Naturally, OECD standards are designed with the interests of rich countries at heart, but the OECD is reaching out to developing countries in order to try to retain its dominant status in the world of international tax.

United Nations (UN)

The United Nations Committee of Experts on International Cooperation in Tax Matters, a part of the Economic and Social Council (ECOSOC), is the other important body in the field of international tax. With a mandate to specifically consider the interests of developing countries, the committee also has a model tax treaty, which differs from the OECD’s in ways that give developing countries much more scope to tax MNCs.

Because it is a committee of experts, not an intergovernmental body, the UN Committee’s status is perhaps lower than that of the OECD, and its members have no formal mandate from their countries. All that may change in 2011, as the G77 group of developing countries push for the committee to be upgraded through ECOSOC.

Lawyers/legal bodies

Much like accountants, lawyers are a vital profession for upholding the integrity of the laws that govern countries. Tax lawyers can negotiate good tax treaties, but some engage in drafting the laws that enable large corporations and wealthy individuals to keep their earnings and assets tax-free. Some lawyers also manage and create trust accounts for their clients, and sometimes actively promote secrecy jurisdictions and tax havens to their clients.

The judiciary

The judicial system interprets the law, and constitutes the legal branch of the government, including all of the courts. A public prosecutor may charge serious tax offenders and tackle corruption and bribery, as well as money laundering – meanwhile, inactivity may slowly erode the tax morale.

Bankers

The banking secrecy laws of jurisdictions such as Austria, Dubai and Switzerland, as well as financial secrecy in Jersey, Guernsey and the Cayman Islands, prevent tax authorities from tracing suspected tax fraud or corrupt flight of wealth. While banks play a crucial role in facilitating credit and savings for individuals and businesses, some banks have been found to be major facilitators of corruption, tax evasion and other types of illicit financial flows.

High net worth individuals

In most countries, the keenest individual tax avoiders fall into the category of those who have over US$1 million in financial assets. Worldwide there are about 10 million such persons, while Africa has around 860,000 rich individuals with a combined fortune of US$747 billion8 in personal wealth. South Africans account for over half this wealth. An estimated 30 per cent of global individual wealth remains permanently offshore which, unless declared, won’t be taxed as it is hidden in secret accounts.

Trade unions

Trade union members are also ordinary taxpayers, and so these organisations often engage in political debates around tax policy. In many countries, they fight regressive taxes

such as VAT, as well as calling for higher and more effective taxation of high net worth individuals and businesses. They can be useful allies for tax justice advocates.

Human rights groups

There is a strong relationship between tax dodging and corruption. For example, tax evasion involves breaking the law and ensuring that you can get away with it; rich companies and individuals rely on patronage through political elites to ensure that the tax system works in their favour; and tax haven secrecy assists with tax dodging as well as with corruption. Equally, economic rights are violated when states are unable to meet their obligations because of weak or unfair taxation. So on many of the problems that tax justice advocates are trying to solve, as well as on many of the solutions, agendas can overlap with those of human rights groups.

Mapping and analysing your tax stakeholders

The ‘Who’s Who’ section above is designed to give you a flavour of some tax-specific stakeholders. When you come to identifying which stakeholders are relevant to the tax issue you have chosen to work on, it’s helpful to ask the following questions:9

- Which are the relevant groups, professions or organisations?

- What is their specific interest or stake in the tax issue you’re focusing on?

- What is their position in relation to the issue?

Appendix 2 provides a detailed mapping of the key tax stakeholders relevant to the issue of country-by-country reporting, in a table that is designed to answer the above questions. You could consider compiling a similar table, inserting the stakeholders that are relevant to whichever tax issue you are working on.

Once you’ve mapped out the stakeholders relevant to tax, you could do some more detailed analysis of these stakeholders by using the tool below: the stakeholder analysis table. This will help you understand the importance of the issue to each stakeholder and their level of influence over the change you want to see. It will help you identify:

- how much each group agrees with your position (on a scale of L = low, M = medium, H = high level of agreement)

- how important the issue is to them (on a scale of L = low, M = medium, H = high priority)

- what level of influence they have over the specific issues (on a scale of L = low, M = medium, H = high level of influence).

TOOLStakeholder analysis table10

Stakeholder | What interest do they have in this issue? | To what extent do we agree on the issue? | How important is this issue for them? | How much influence do they have? |

Those directly affected: poor citizens | They spend a large proportion of their income on goods and services that will now be taxed: more as a proportion of their income than the wealthiest. So the tax will make them poorer. | L M H Affected the most severely and the core group we work with | L M H Due to major impact | L M H Government prone to neglect voice of poorest in society though potential for change if effectively mobilised |

Government and state decision-makers Ministry of Finance Revenue Authority | They need to raise revenue for services and infrastructure, but | L M H Low to medium as we share the aim of reducing aid dependency and increasing tax intake, but we object to regressive nature of this tax, manner of roll-out and level it’s set at | L M H Due to concessions given to extractives not generating enough income, need money to invest in infrastructure, etc | L M H In charge of tax policy with strong influence from president’s office |

Civil society organisations: Tax Advocacy Coalition (including NACE and BAN) | These CSOs have long advocated for fairness and transparency in government accounts and for greater accountability of the extractives sector. They are part of a coalition that has started to look into tax issues more generally in Sierra Leone, including asking the government to reduce the new GST from 15 per cent to 10 per cent. | L M H Natural allies | L M H They see this as a key development issue | L M H Currently low but scope to enhance influence once mobilised |

UK Department for International Development (DFID) | DFID is a big player and has invested a lot of resources in GST roll-out, tax collection, etc. | L M H Agree there’s a need to improve tax policy and reduce dependence on aid, but CSOs think rate too high and lack clarity on which sectors will benefit. DFID unhappy about challenge from some CSOs | L M H They have invested a lot of resources, both financial and political | L M H A major development player in Sierra Leone |

Key: L = Low M = Medium H = High | ||||

Analysing the policy context and opportunities

In addition to analysing who has power over your issue and/or who has a stake in it, you

will also need to analyse what policies and policy processes you need to influence in order to bring about the changes you are seeking – particularly at the national level. National policy-makers, for example, cannot operate in a vacuum. Even if you manage to persuade them of the need for change on a given issue, they can only bring about that change through established policy or legislative channels and processes. If you do not relate your proposals for change to specific political opportunities or policy processes available to policy-makers in your country, you are likely to be ignored.

The following are key questions to address in your analysis of the policy context:

- What are the different policies that impact on the problem or situation you are trying to address?

- Which are the policies that have the most impact on the problem and could most help solve the problem if they were changed? (this will help you prioritise where to focus your advocacy work)

- What is the current status of the policy you will seek to change? Is it enshrined in law? Or is it simply the adopted policy or position of the current government?

- What are the mechanisms for bringing about a change in the policy? (these could be local, national, regional or international – or a combination)

- How have changes to this policy been brought about in the past in your country?

- Are there opportunities for changing the policy in the near future (for example, a parliamentary bill on the extractives sector, or a general election)?

- How and where can you access further information about a policy?

Analysis of the policy context for your advocacy is not something you do just when you are first developing your advocacy strategy. It has to be ongoing throughout the course of your advocacy strategy, as politics and policies are always changing – regardless of your advocacy! For example, a general election and a change of government can change the policy context for your advocacy overnight.

For further advice and support on analysing the policy context for your advocacy, see Monitoring Government Policies: A Toolkit for Civil Society Organisations in Africa by Cafod/Christian Aid/Trocaire

(http://cdg.lathyrus.co.uk/docs/MonitorGovPol.pdf)